Many Smaller SMBs Opt to Process Ad Hoc Payments Manually — and It’s Costing Them

Fifty-seven percent of the total accounts receivable (AR) transactional volume flowing into the coffers of small to mid-sized businesses (SMBs) comes in the form of nonrecurring, ad hoc payments.

Yet, PYMNTS Intelligence found that in most cases, the process around receiving and processing these ad hoc payments is far from efficient. Delays are common, and those delays can result in cash flow shortfalls — which can be especially detrimental to smaller firms.

In PYMNTS Intelligence’s “How Instant Ad Hoc Payment Costs Impact Small SMBs,” a collaboration with Ingo Payments, we determined one way many SMBs are overcoming these inefficiencies and delays is by leveraging the use of instant payment methods. Doing so enables SMBs to turn ad hoc payments more quickly into working capital, which is especially important to those small SMBs who are the primary receivers of ad hoc payments.

Ad hoc payments make up 72% of SMBs’ AR volume in dollars, and using instant payment methods can provide them with timely receipt of their funds. This likely explains why the share of ad hoc payments received instantly rose 24% since September 2023.

However, for many SMBs, the cost of processing instant payments can be prohibitive. The smallest SMBs — those generating less than $100,000 in revenue annually — have decreased their use of instant payments since September 2023, we found, likely because of the fees associated with processing instant payouts.

But PYMNTS Intelligence data suggests that those SMBs that opt to process ad hoc payments manually — because they believe they are saving money by doing so — may ultimately be misguided.

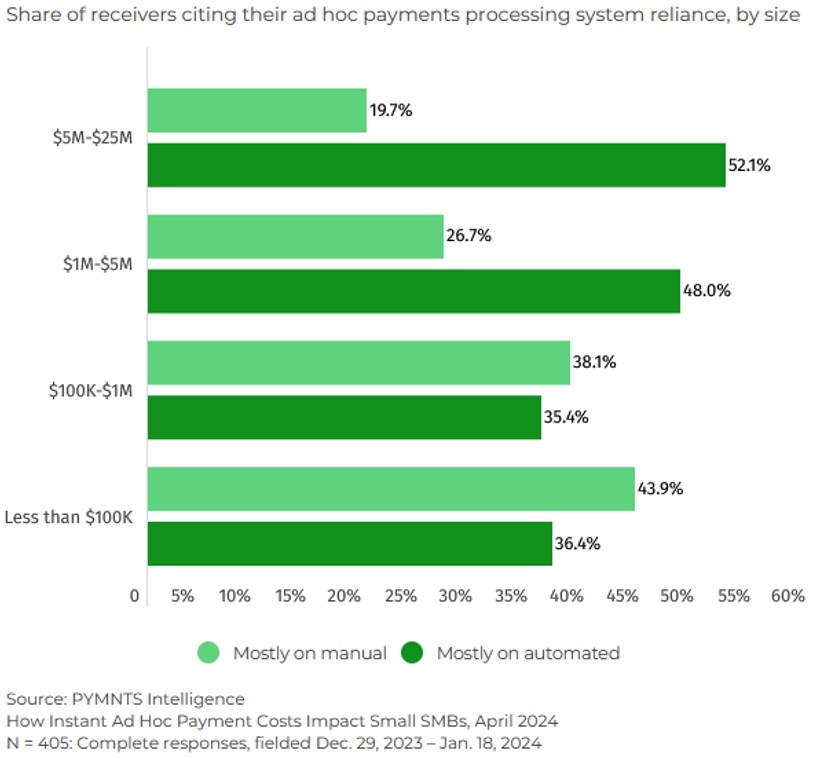

In exclusive PYMNTS Intelligence data was not included in the final edition of “How Instant Ad Hoc Payment Costs Impact Small SMBs,” we found that the smaller the SMB is, the more likely it was to process ad hoc payments manually.

As the chart illustrates, 44% of SMBs earning less than $100,000 annually rely mostly on manual methods of processing their ad hoc payments; 38% of those earning between $100,000 and $1 million annually do the same. Meanwhile, 52% of those SMBs earning between $5 million and $25 million annually and 48% of firms earning between $1 million and $5 million rely primarily on automated ad hoc payment processing.

This reliance on manual processing is especially important to note because firms that rely on internal, manual processes actually pay the highest fees: $12.70 per transaction, or 9% more than what SMBs relying primarily on automated systems pay.

In other words, when smaller SMBs do pay to process their ad hoc payments instantly, they pay more, which likely reinforces their fee-averse position.

But by incorporating external vendors and intermediaries to process ad hoc payments instantly, fee-averse SMBs could actually lower their overall costs in the end.

PYMNTS Intelligence found that 57% of SMBs overall are now willing to pay a fixed fee to receive instant payments, while one-quarter of the smallest identify the expense associated with instant payments to be the biggest barrier in their adoption of instant payment processing.

The lesson here is twofold: It’s costing smaller, fee-averse SMBs more to process their ad hoc payments manually. Meanwhile, those senders looking to enhance their relationships with smaller SMBs might be missing an opportunity to do so by offering them free or low-cost instant payouts for ad hoc payments.

The post Many Smaller SMBs Opt to Process Ad Hoc Payments Manually — and It’s Costing Them appeared first on PYMNTS.com.