The Future of Credit Is Clashing With Its Past

Consumer credit has so far been shaped and defined by a single product. The revolving credit card.

But the revolving credit card’s fundamental architecture, built for a world where credit lines were static and repayment schedules predictable, is now colliding with a new consumer reality.

Findings in the March 2026 edition of the Payments Innovation Tracker® Series, a PYMNTS Intelligence collaboration with Paymentology, reveal that consumers increasingly expect credit to behave like software: flexible, responsive and tailored to specific purchases or financial situations.

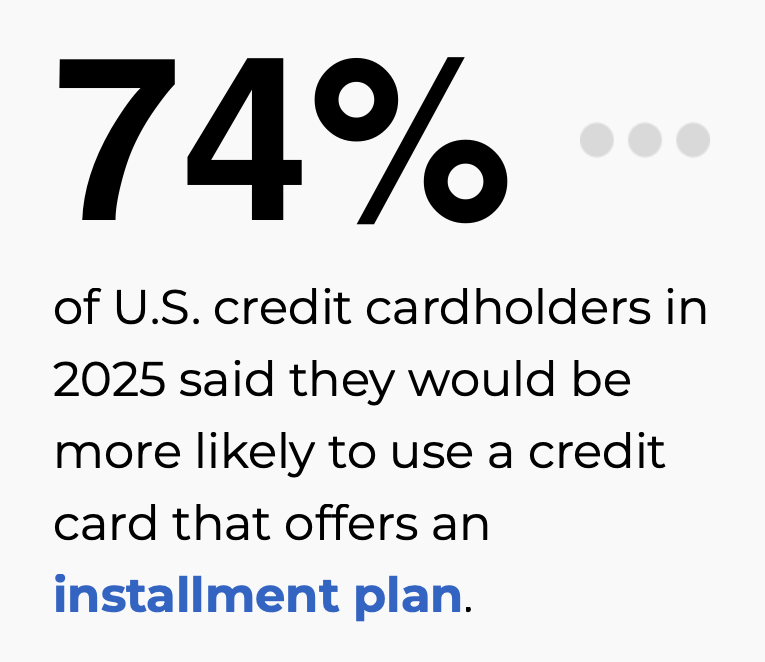

Today’s credit card holders increasingly want the ability to split transactions into installments, shift due dates to align with pay cycles, and access financing embedded directly into everyday transactions, from travel bookings to retail checkouts.

This shift is forcing a structural rethink inside banks and fintech companies alike. The result is increasingly emerging as a credit infrastructure reset: a move away from fragmented, batch-based lending systems toward unified, real-time platforms that treat credit not as a static product but as programmable financial infrastructure.

After all, as the report highlighted, 45% of all credit cards are expected to be issued on unified infrastructure by the end of the decade.

Overcoming the Limits of Legacy Lending SystemsThe technological component of the credit landscape’s behavioral evolution is the convergence of two previously distinct models of consumer borrowing: traditional credit cards and buy now, pay later (BNPL) financing.

For years, the BNPL sector positioned itself as a disruptive alternative to credit cards, offering fixed installment payments at the point of sale. But the market is now evolving toward something more nuanced. Instead of replacing cards, installment financing is being absorbed into them.

Consumers increasingly expect credit products that can support both revolving balances and structured installment plans within the same account. A large purchase might be converted into a six-month payment plan, while everyday spending continues on a revolving basis.

From a customer perspective, this hybrid model offers flexibility and control. From an infrastructure perspective, however, it introduces complexity that traditional card systems were never designed to manage. Installment conversions, dynamic credit limits and event-triggered offers require far more sophisticated orchestration between transaction processing, credit ledgers and lending decision engines.

Read the report: The Credit Reset: How Unified Platforms Are Replacing Legacy Lending Infrastructure

Banks may have the capital, customer base and regulatory expertise to compete aggressively in consumer lending, but outdated infrastructure can make it difficult to experiment with new product models or respond quickly to changing consumer expectations.

To close that gap, financial institutions are exploring unified credit platforms that combine several functions traditionally handled by separate systems.

In these architectures, credit ledgers, payment processing and lending logic operate within a single integrated environment. Transactions, credit decisions and repayment structures can be managed in real time rather than through overnight batch processes.

The deeper transformation underway is conceptual as much as technological.

Historically, credit products were designed as fixed financial instruments: a loan, a card, a line of credit. The terms were established upfront and changed only occasionally. In the emerging model, credit behaves more like a programmable service. Lending terms can adjust dynamically in response to transactions, customer behavior or contextual factors.

In that sense, the credit reset is not simply about technology modernization. It represents a broader shift toward a future where lending operates with the same flexibility, speed and programmability that now define much of the digital economy.

At PYMNTS Intelligence, we work with businesses to uncover insights that fuel intelligent, data-driven discussions on changing customer expectations, a more connected economy and the strategic shifts necessary to achieve outcomes. With rigorous research methodologies and unwavering commitment to objective quality, we offer trusted data to grow your business. As our partner, you’ll have access to our diverse team of PhDs, researchers, data analysts, number crunchers, subject matter veterans and editorial experts.

The post The Future of Credit Is Clashing With Its Past appeared first on PYMNTS.com.