75% of Financially Stable Consumers Prefer Co-Branded Cards for Rewards

Higher costs and financial uncertainty are prompting many consumers to reassess their credit card choices. Financial stability plays a key role in how individuals select their cards, with factors like rewards and credit-building opportunities influencing their decisions.

According to a PYMNTS Intelligence report, “Consumers’ Financial Health and Spending Priorities Guide Credit Card Choices,” a collaboration with Elan, spending behavior remains consistent, regardless of a consumer’s financial situation or the purpose behind opening a new card.

General-Purpose Cards Dominate Consumer PreferencesMost consumers, including those who already own credit cards, opted for general-purpose cards when opening new accounts in the past year, according to the report. About 66% of consumers chose general-purpose credit cards, with financially stable individuals more likely to hold such cards. In contrast, co-branded cards, often linked to specific retailers or brands, were less popular, especially among financially struggling consumers.

While 75% of financially stable consumers leaned toward co-branded cards, only 39% of those struggling financially chose this option. This suggests financially secure consumers tend to prioritize rewards and benefits tied to their everyday purchases, while those with tighter finances tend to select more flexible options.

Recommendations Influence Decision-MakingThe report also highlights the role personal recommendations plays in credit card selection, as 73% of consumers who received recommendations from family or friends found them highly influential in their decisions. This trend was especially noticeable among financially stable individuals (75%) compared to their struggling counterparts (68%).

In terms of financial motivations, the report found financially stable consumers tended to prioritize rewards when selecting a new card, whereas those with less financial security were more focused on building credit or managing emergency expenses. Nearly 26% of financially stable consumers selected a card primarily for rewards, while only 13% of financially struggling consumers did the same.

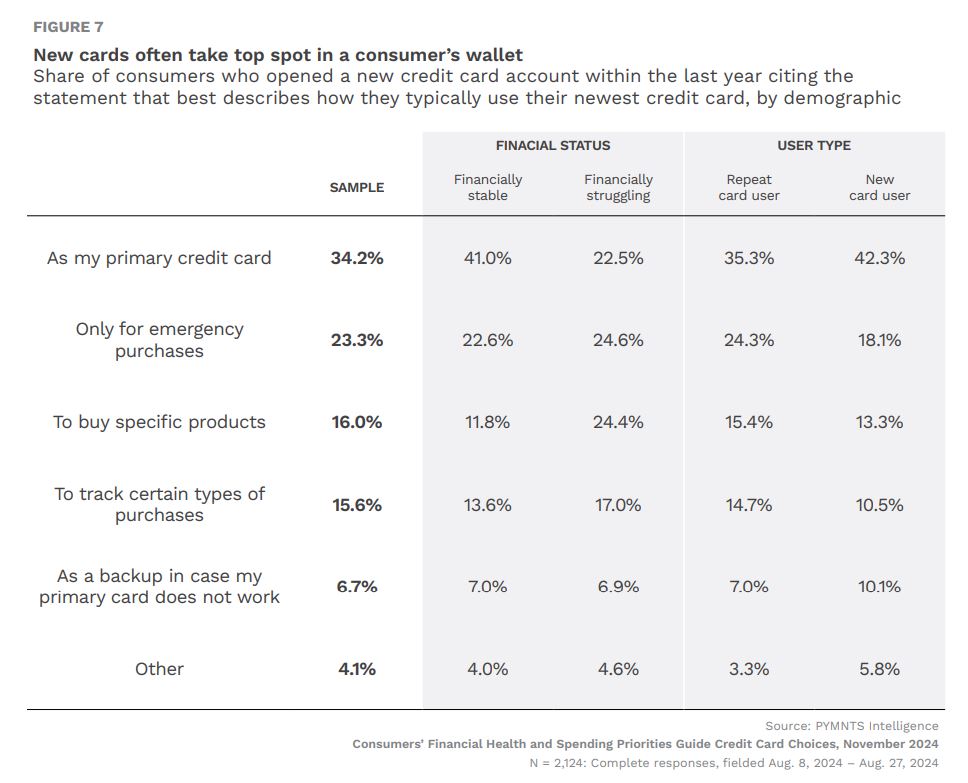

Spending Behavior Consistent Across Financial GroupsDespite differing motivations for acquiring new credit cards, consumers’ spending behaviors were notably consistent. Whether obtaining a card for rewards, credit-building, or emergency purposes, consumers tended to use their new cards actively. Roughly 58% of cardholders reported using their new cards as their primary card or for specific purchases. Both financially stable and struggling consumers spent similarly when it came to rewards-based cards, with average spending at about $1,700 for both groups.

Similarly, emergency-related spending was almost identical, with stable consumers averaging $1,974 and struggling consumers at $1,824. This suggests that, while motivations for getting a new card vary, spending patterns once the card is obtained are largely unaffected by financial status.

Consumer credit card choices are shaped by financial health, recommendations, and spending intentions. Financially stable individuals often seek rewards and co-branded cards, while those facing financial struggles prefer general-purpose options. Regardless of their financial situations, most consumers use their new cards for active spending, not occasional purchases. These insights highlight the impact of financial health on credit card decisions and spending behaviors.

The post 75% of Financially Stable Consumers Prefer Co-Branded Cards for Rewards appeared first on PYMNTS.com.