US BNPL Transactions Hit $175 Billion Amid Shifting Consumer Demands

The traditional pillars of consumer credit are undergoing a profound transformation as “pay later” options, once a niche for specific shoppers, are now redefining how Americans spend and borrow.

A new PYMNTS Intelligence report, “Pay Later Revolution: Redefining the Credit Economy,” highlights this evolution, detailing an ecosystem where traditional banks, nonbank lenders and FinTech startups are both competing and collaborating to offer flexible financing solutions for a widening array of goods and services. From the emergence of metal charge plates in the early 20th century to today’s digital wallets and buy now, pay later (BNPL) models, the industry is fundamentally altering consumption patterns for millions.

Today’s pay later market is characterized by changing consumer preferences for predictability in managing spending and borrowing, driving the rise of alternative credit providers with innovative underwriting and lending models. These providers have demonstrated the value consumers place on certainty regarding loan payoff over a specific period. The ecosystem now encompasses a broader cohort of consumers beyond those with limited credit, including individuals with established credit profiles who use these options for financial optimization.

Traditional banks, once the dominant players in consumer lending, are actively adapting their infrastructure, developing their own installment options and forming partnerships with FinTech alternatives to retain customer loyalty and remain central to financial lives. The report identifies five key themes for 2025: the growing consumer appeal for predictable installments, the pressure on banks to integrate installment options earlier in the shopping journey, the blurring lines between short-term and long-term BNPL products, BNPL business models increasingly resembling traditional credit card models with a focus on consumer fees, and a coming convergence between traditional credit and pure-play BNPL providers driven by the demand for payment optionality embedded at checkout.

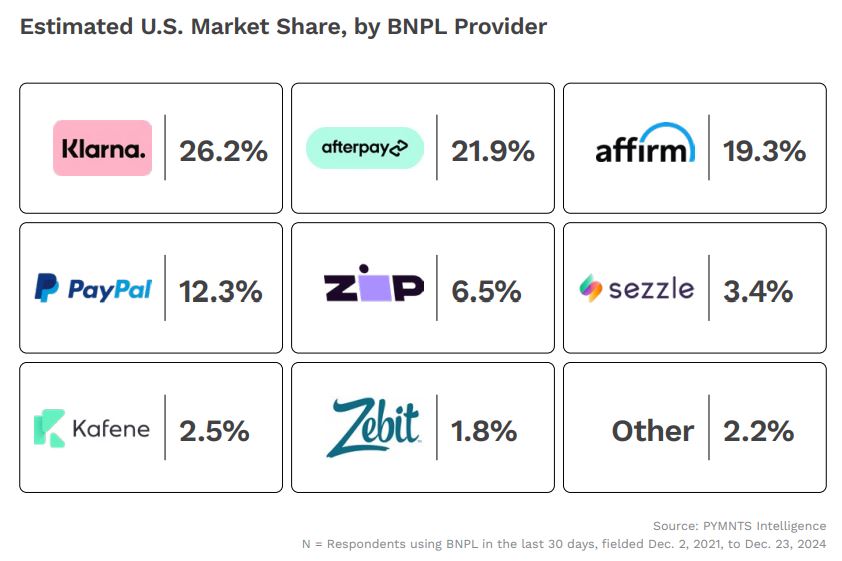

Key data points from the report include:

- 128 million adult Americans used a pay-later product from at least one alternative credit provider over the last 12 months.

- U.S. BNPL transactions currently total $175 billion.

- As of mid- to late January 2025, nearly 30% of all BNPL loans were past due.

Beyond the structural shifts and key market indicators, the report also delves into the differing consumer profiles utilizing pay later — classifying users by necessity due to limited traditional credit access versus convenience for cash flow management and financial optimization. It examines the complex flow of funds and diverse revenue models, highlighting the shift from purely merchant-funded approaches to hybrid models incorporating consumer fees like interest, late charges and subscriptions.

The analysis further touches on the critical roles played by ecosystem stakeholders, including merchants, technology infrastructure providers, payment networks and regulators. The report discusses the uncertain regulatory landscape, noting the potential for increased state-level oversight and the impact of agencies like the CFPB, FinCEN, OCC, FDIC, FTC and Federal Reserve on the evolving industry. Finally, the report highlights the influence of artificial intelligence (AI) in reshaping underwriting, fraud prevention and customer experience.

The post US BNPL Transactions Hit $175 Billion Amid Shifting Consumer Demands appeared first on PYMNTS.com.