Half of Stable Mid-Market Firms Use Credit as Growth Capital

Middle-market companies are caught between tariffs, interest rates and jittery supply chains, and how they borrow money says as much about their outlook as their balance sheet.

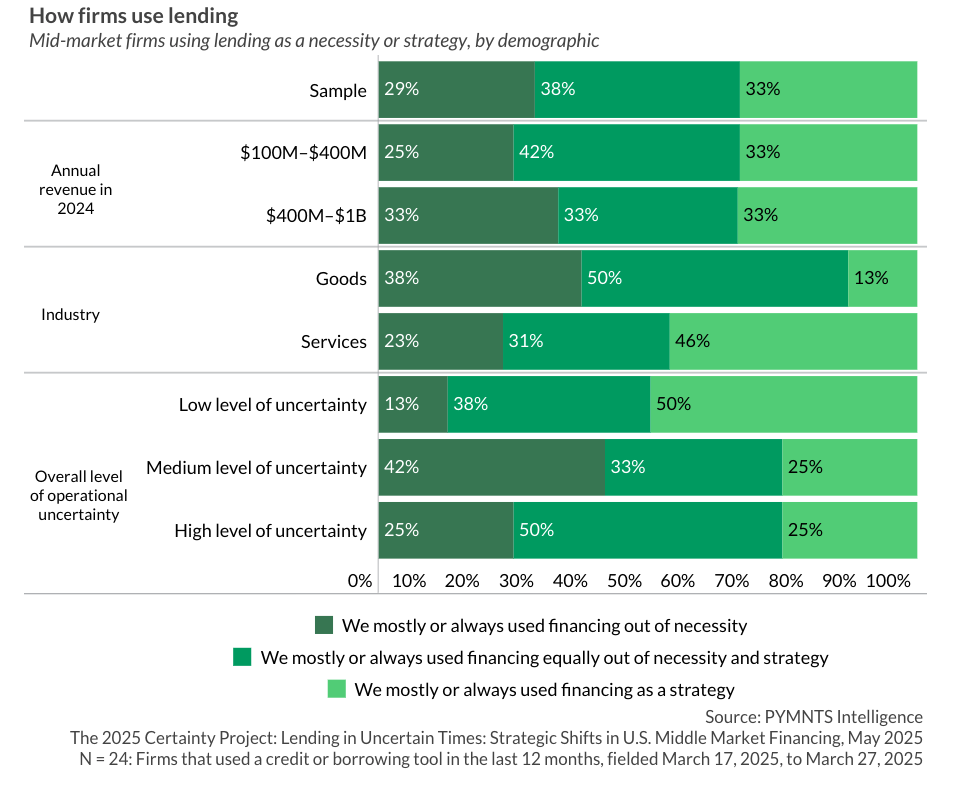

The PYMNTS Intelligence report “Lending in Uncertain Times: Strategic Shifts in U.S. Middle-Market Financing,” part of The 2025 Certainty Project, surveyed 60 payment executives at companies with revenues between $100 million and $1 billion. It found that while embedded lending promises speed and convenience, mid-market firms still cling to the predictability of traditional bank loans when the business climate looks shaky.

Firms’ financing choices hinged less on credit availability than on how much confidence managers had in their operations. Traditional credit remained the dominant option, but the report showed that embedded lending is starting to carve out a niche, especially among companies with a steadier footing.

- Confidence drives strategy: Half of firms operating in stable conditions reported using financing primarily as a growth lever to build inventory ahead of demand or finance expansion. Only 1 in 4 firms facing high uncertainty said the same.

- Embedded lending lags: Only 20% of firms overall preferred embedded loans, with enthusiasm peaking at 32% among low-uncertainty firms. Just 7% of high-uncertainty firms favored the option, underscoring a trust gap between new platforms and traditional banks.

- Motivations diverge: One-third of firms under pressure cited faster approvals as the main draw of embedded lending. By contrast, firms in calmer waters valued the ability to streamline cash flow management and reduce paperwork.

The findings highlighted a tension at the heart of corporate borrowing. Embedded lending, which integrates credit into platforms such as eCommerce sites or accounting software, is designed to be frictionless. But for executives accustomed to clear terms and established compliance, its speed can feel like a tradeoff against transparency. High-uncertainty firms, in particular, gravitated to bank loans because repayment schedules and interest rates are predictable, even if paperwork is slower.

That leaves embedded lenders with a marketing and product challenge. They are tasked with tailoring offerings not just by industry or size but by operational certainty. A one-size-fits-all approach risks alienating cautious and confident borrowers. For firms playing defense, faster approvals may be the hook. For stable operators, better integration with back-office systems and flexible terms could help build trust.

The study also revealed how industry context shapes financing behavior. Goods producers, for example, reported turning to financing out of necessity more than their service-sector peers, a sign of how tariffs and global supply snags amplify uncertainty. Meanwhile, firms in more stable environments treated loans as leverage, not lifelines, a subtle but telling distinction in how credit markets are evolving.

Traditional finance, with its longer repayment horizons and larger credit limits, is unlikely to lose its grip soon. Embedded lending’s adoption curve will depend on whether providers can close the transparency gap and prove they can offer speed and safety.

Until then, the story of mid-market borrowing will remain one of cautious experimentation at the edges, with banks still the backbone in uncertain times.

The post Half of Stable Mid-Market Firms Use Credit as Growth Capital appeared first on PYMNTS.com.