Global Easing Hits 35-Year High—So Why Is Bitcoin Still Flat?

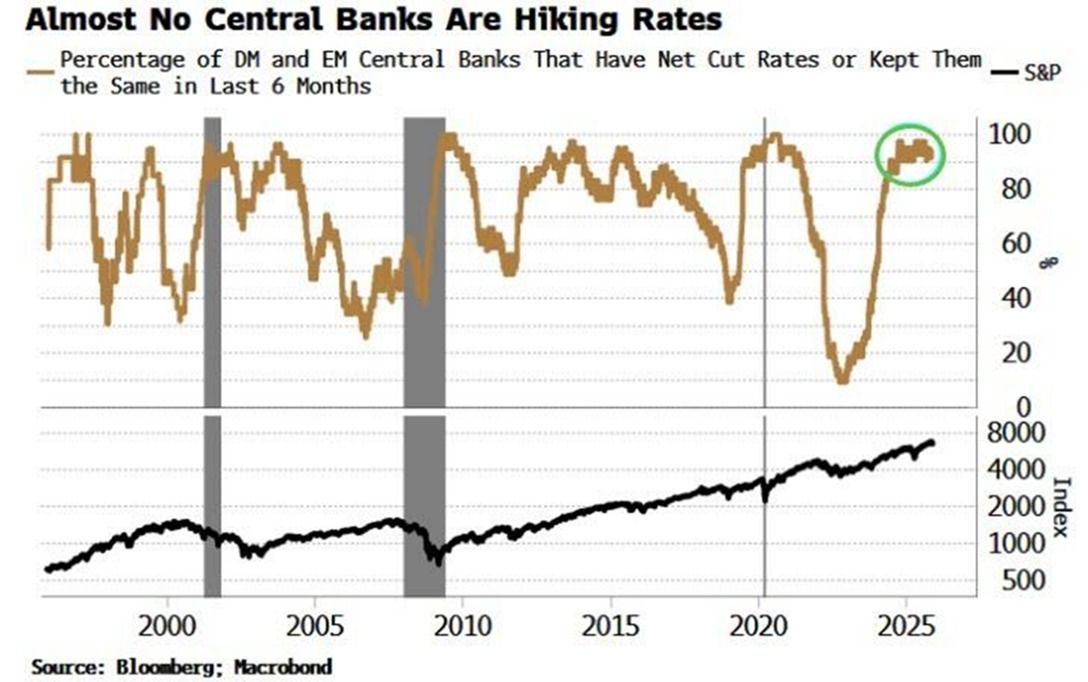

More than 90% of the world’s central banks have cut rates or held them steady for 12 straight months, a pattern rarely seen in the past 35 years. This easing cycle has produced 316 rate cuts over two years, topping even the 313 seen during the 2008–2010 financial crisis.

Despite this global expansion of liquidity, Bitcoin has decoupled from growth in the money supply since mid-2025. This trend prompts questions about when the leading cryptocurrency will respond to the influx of capital.

Unprecedented Monetary Easing Since the PandemicGlobal monetary policy has entered its most aggressive easing phase since the COVID-19 pandemic, based on data from The Kobeissi Letter. Fewer than 10% of central banks have increased rates, with most cutting or maintaining policy. This trend has persisted for a year, marking a rare global monetary pivot.

The extent of this easing is clear when looking at cumulative rate cuts. From 2023 through early 2025, central banks in both developed and emerging markets have cut rates 316 times—surpassing the 313 cuts between 2008 and 2010, when the global financial system was under severe duress.

Chart showing the percentage of central banks that have cut or held rates over the last 6 months. Source: The Kobeissi Letter

Chart showing the percentage of central banks that have cut or held rates over the last 6 months. Source: The Kobeissi Letter

Historically, coordinated monetary easing has preceded notable increases in asset prices, especially in risk assets such as stocks and cryptocurrencies. Yet Bitcoin’s response to this liquidity wave has been much more muted than in previous cycles. While earlier research found a 0.94 correlation between Bitcoin’s price and the global M2 money supply (from May 2013 to July 2024), that connection appears temporarily weakened now.

This decoupling raises questions about timing and market drivers. Analysts observe that Bitcoin often lags global liquidity increases by 60 to 70 days. Should this historical pattern persist, the ongoing monetary expansion could delay a Bitcoin rally until late 2025 or 2026.

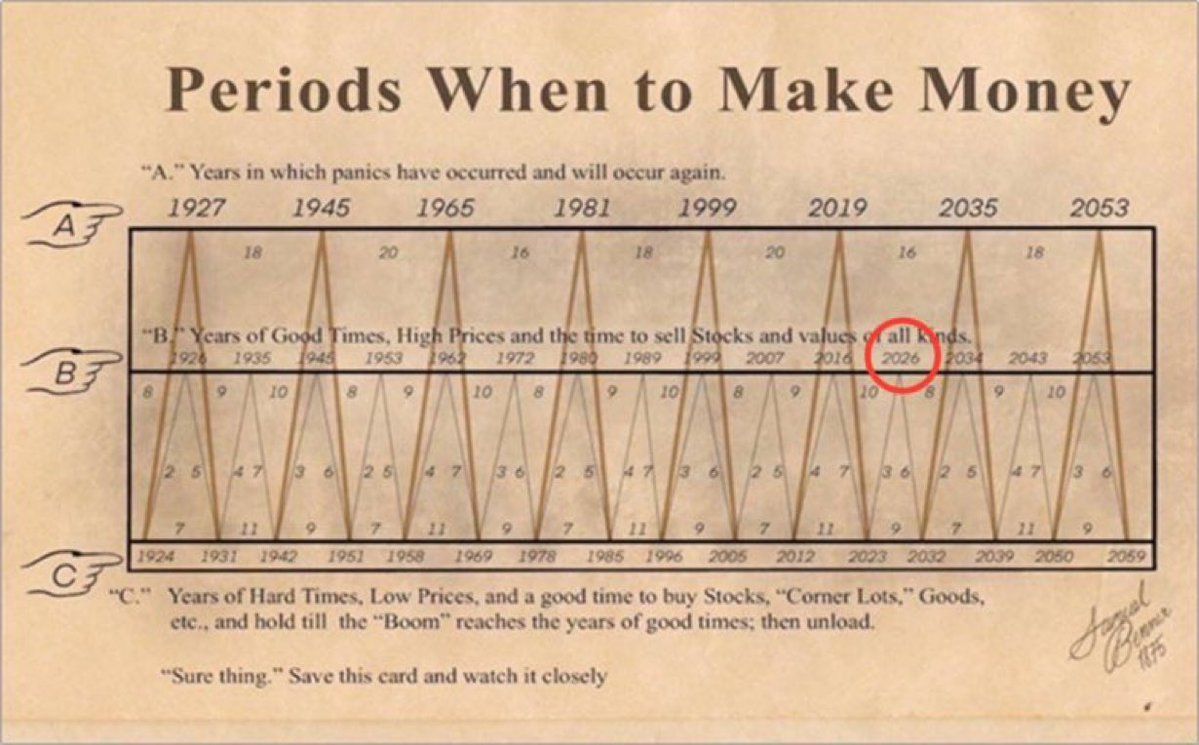

2026 Financial Shock ScenarioMarket watchers outline a possible scenario unfolding through 2028, with 2026 as a turning point. This matches the historical cycles described by the Benner Cycle, a 19th-century market timing model that has surprisingly forecast many financial pivots.

The Benner Cycle chart highlights 2026 as a year of ‘good times’ and a potential market peak. Source: Quinten François

The Benner Cycle chart highlights 2026 as a year of ‘good times’ and a potential market peak. Source: Quinten François

According to market analyst NoLimitGains, several global stress points are converging toward 2026. Fault lines include US Treasury funding issues, Japan’s yen carry-trade risk, and China’s heavy credit leverage. Disruption along any of these would create global shocks, but simultaneous problems could drive a systemic crisis.

Phase one is defined by a Treasury funding shock, possibly triggered by weak US bond auctions. The US faces record debt issuance in 2026 as deficits grow and foreign demand declines. Weak auctions and fading indirect bids echo the UK’s 2022 gilt crisis. Dollar surges, liquidity disappears, Japan intervenes, yuan drops, credit spreads widen, risk assets sell off, etc.