Data Shows Most Consumers Are Managing Credit Despite Pressures

The conventional wisdom is that consumers in the United States, burdened by debt, are trapped in a cycle of using credit to get what they need, and then juggling their debt, grappling with monthly payments.

[contact-form-7]But data and commentary from earnings season thus far indicate that most consumers are proving to be adroit managers of credit, particularly credit cards.

Although delinquencies have been on the rise, depending on where you look, they’re coming off a small base, and individual firms are reporting stable-to-improving credit metrics as they weigh in with their latest quarterly reports.

By the NumbersThe Federal Reserve Bank of New York reported this week that national household debt reached $18.4 trillion in the second quarter of 2025, increasing by $185 billion. This represents a 1% rise from the first quarter of the year and a 3.3% increase compared to the same period in 2024. Mortgage balances are roughly 71% of the tally.

Credit card debt rebounded and almost fully reversed declines recorded in the first quarter. In the second quarter, it reached $1.2 trillion, nearly matching the peak observed in the final quarter of 2024. Student loan balances continued to climb for the fourth straight quarter, reaching $1.6 trillion, which is $7 billion higher than in the first quarter. Altogether, non-housing balances rose by $45 billion, representing a 0.9% increase from the previous quarter.

Delinquency rates increased slightly compared to the first quarter. The report showed that 4.4% of outstanding debt is in some stage of delinquency, up from 4.3% last quarter and marking the highest level since 2020. Serious delinquencies, defined as debt that is 90 days or more past due, rose to 3% percent of total debt. This represents a 6.8% increase from the previous quarter and a 65% rise year over year. The last metric reads as an alarming one, but the read-across is that 97% of debt is not in that troubled stage.

The increase was mainly driven by student loans, which are now out of a repayment pause that stretched out over five years. In the second quarter, 10.2% of student loan balances were seriously delinquent, a 31% increase from the previous quarter.

However, the share of mortgages, HELOCs and credit card balances in serious delinquency decreased, falling to 0.82%, 0.85% and 12.2%, respectively.

Young Consumers Bear WatchingWhen examining the data by age group, debt among consumers younger than 30 years old rebounded, reaching $1.11 trillion after falling to $1.05 trillion in the previous quarter. Consumers in their 30s and 40s also experienced an increase in debt balances. These three age groups have the highest share of individuals in serious delinquency. Among consumers under 30, 4.6% are seriously delinquent. This figure is 37% higher than what was recorded in the first quarter and is the highest since 2017. Among consumers in their 30s, 3.5% are seriously delinquent. This rate has doubled compared to the same period last year and is now at its highest level since 2014.

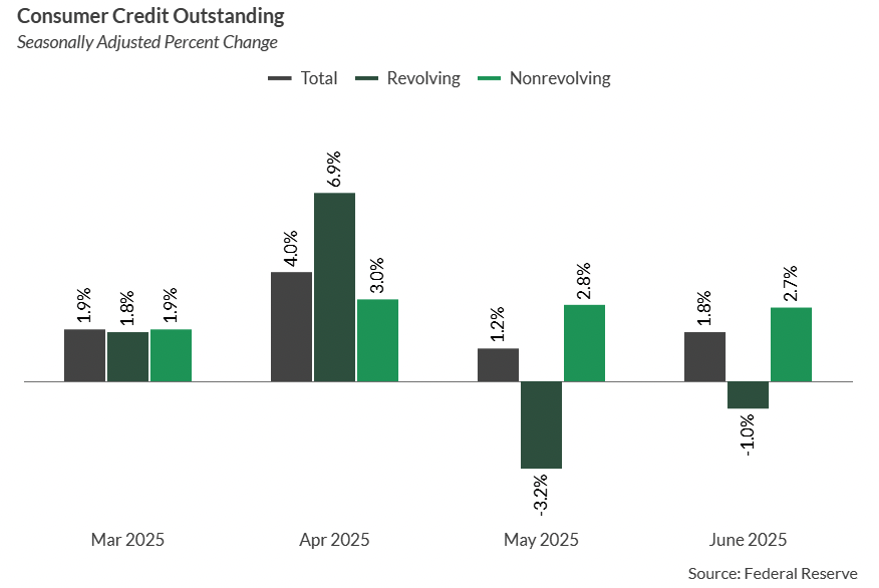

The Day-to-Day Debt ManagementIn another report from the Federal Reserve, known as G19, in the second quarter, consumer credit grew at a seasonally adjusted annual rate of 2.3%, marking an acceleration from the 1.2% pace in the first quarter. In June, total consumer credit rose at a 1.8% annualized rate, bringing the outstanding balance to $5.01 trillion, matching the highest level since November 2024. Compared to June 2024, outstanding credit increased by 2.1%.

There is evidence that consumers are chipping away at card balances. Revolving credit — a category that includes but is not limited to cards — edged down at an annual rate of 1% in June, following a 3.5% decline in May.

There’s reason to think that young consumers are not the lost generation when it comes to using credit. As Karen Webster wrote in a Wednesday (Aug. 6) column, citing PYMNTS Intelligence data, “Gen Z saves 36% of their income, 10 points more than older generations. But they don’t just stick it in a checking account. They diversify. Some of it goes to digital wallets. Some into high-yield savings. Some into crypto.”

“Gen Z understands the power of credit,” she added. “They’ve watched credit scores shape everything from car loans to job offers. So, they use credit with intent.”

Generation Z is nearly three times more likely to use credit-builder products than older consumers, she wrote, which in turn indicates an awareness and desire to cement responsible habits.

Payment networks have weighed in, too, with earnings results that showed debit spending largely outpacing credit volumes, which would indicate some prudence and shifting in payment behaviors, using cash on hand.

Elsewhere, during JPMorgan’s earnings call July 15, Chief Financial Officer Jeremy Barnum told analysts: “If you look at indicators of stress, not surprisingly, you see a little bit more stress in the lower-income bands than you see in the higher-income bands. But that’s always true… And nothing there is out of line with our expectations. Our delinquency rates are also in line with expectations … all of that looks fine.”

The post Data Shows Most Consumers Are Managing Credit Despite Pressures appeared first on PYMNTS.com.