BNPL Gets Boost From Bank Partnerships and Use in Credit Scoring

Earlier this year, PYMNTS Intelligence detailed that pay-later options were drawing widespread use among consumers versus payments via traditional credit cards.

The data showed that coming into the end of 2024, 56% of consumers used installment payment options in the last year. Within the various pay-later offerings, buy now, pay later (BNPL) was a standout, as 76% of BNPL users said they were highly satisfied with the experience of using BNPL to make everyday purchases and large-ticket transactions.

About 38% of consumers used BNPL, roughly at parity with those who used general-purpose credit card installment plans and above the 24% that used BNPL in the previous year. In the meantime, the use of credit card installments was static over that timeframe.

The implication, then, is that BNPL is gaining share within the pay-later sphere. Separate data showed that BNPL services appeal to those looking for immediate access to credit without long-term commitments, a factor cited by 27% of individuals.

The Consumer Financial Protection Bureau announced its own findings on BNPL last month.

“Before first-time BNPL use, consumers’ average credit card utilization rates increased, suggesting that less available credit card liquidity may encourage consumers to use BNPL,” according to a Jan. 13 press release.

Liquidity is constrained, as PYMNTS found that 19% of overall consumers hit their credit card limits in the past year — a percentage that soared to 41% of consumers who live paycheck to paycheck with issues paying bills. The constraints are even across income levels, as 20% of those earning more than $100,000 annually and nearly 21% of households earning less than $50,000 annually have been maxing out their cards.

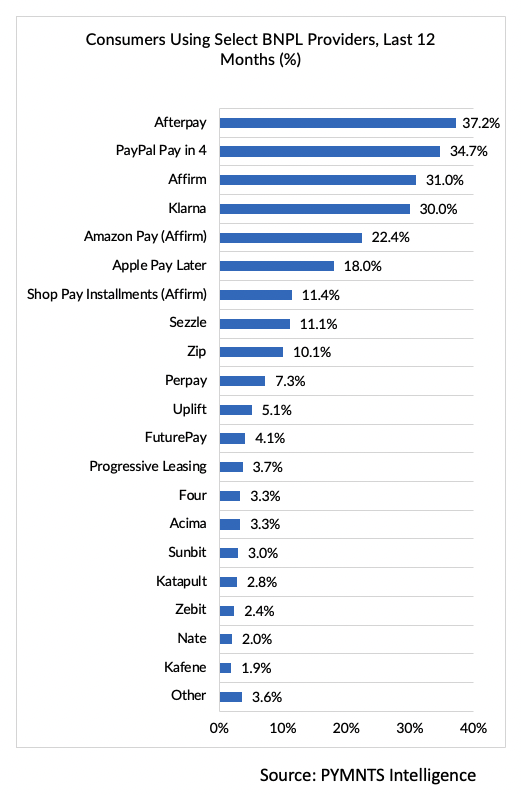

The marquee names in BNPL are gaining the lion’s share of BNPL transactions, as about one-third of consumers who opt to use the payment method go to Afterpay, PayPal, Affirm and Klarna.

The use of BNPL will see additional momentum, in part because of traditional financial institutions — firms that traditionally would have looked askance at BNPL, as it offered an avenue through which customers would bypass using issuers’ cards.

J.P. Morgan and KlarnaAs reported last week, J.P. Morgan Payments is expanding its BNPL offerings in partnership with Klarna. The collaboration lets roughly 900,000 businesses offer Klarna’s installment payment options to customers who use the bank’s payment operations, which process $2 trillion in payments annually.

Specifically, a Feb. 11 press release said the joint efforts will include interest-free BNPL and flexible financing options, available on the J.P. Morgan Payments’ Commerce Solutions Platform. By extension, the announcement with Klarna conceivably tightens J.P. Morgan’s relationship with merchant clients, while opening additional revenue streams.

Elsewhere, FICO said this month that it is planning to add BNPL data to its credit score analysis, having conducted studies with Affirm into BNPL usage. The research showed that if incorporated into its FICO scoring system through a simulation, BNPL helped improve FICO scores while “improving model risk performance for lenders.”

“Based on learnings from this industry-leading analysis, FICO is developing a solution to introduce its proprietary treatment of BNPL data to the credit-scoring marketplace,” FICO said.

The post BNPL Gets Boost From Bank Partnerships and Use in Credit Scoring appeared first on PYMNTS.com.