30% of US Consumers Fall Victim to Financial Scams

Financial scams have become more sophisticated, targeting individuals through personalized and strategic methods. Scammers are using tools from legitimate businesses to make their scams appear more convincing.

A PYMNTS Intelligence report, “How Scammers Tailor Financial Scams to Individual Consumer Vulnerabilities,” in collaboration with Featurespace, reveals the impact of fraud, detailing the financial and emotional harm to victims and the need for better consumer protection and examining key findings on how scammers target consumers.

Scope of Scams and Victim Demographics

Financial scams are more widespread than previously reported. According to the report, about 30% of U.S. consumers — roughly 77 million individuals — have lost money to a scam in the past five years. This highlights the pervasiveness of these crimes, with most victims losing more than $500, and many experiencing even more significant financial losses. The report also shows how scams affect individuals across various demographics, including age, education and income.

While scams like job search fraud tend to target younger consumers, older generations are more vulnerable to eCommerce scams. For example, baby boomers and seniors are three times more likely to fall victim to fake online shopping schemes than Gen Z. These variations in scam susceptibility demonstrate how scammers tailor their approaches to target different groups based on their specific needs and situations.

A key factor in the rise of scams is how scammers personalize their outreach based on the consumer’s lifestyle and characteristics. This personalization makes scams appear more legitimate and harder to detect.

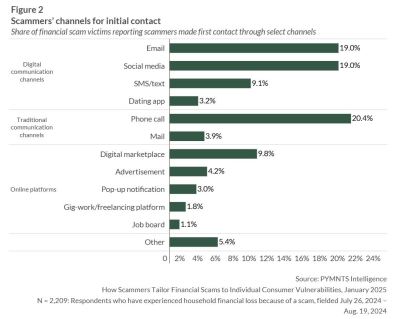

Consider 21% of Gen Z consumers reported falling for scams initiated through social media platforms, reflecting their heavy digital presence. Older generations like boomers are more frequently contacted via email or phone calls, methods they trust more. Scammers often adapt to these preferences, using channels that are most likely to engage specific age groups.

Additionally, scammers personalize their messaging, aligning it with consumers’ fears, aspirations or daily habits. For example, high-income individuals are often targeted with investment scams, while lower-income or less-educated individuals are more likely to fall for government benefits fraud. This type of approach allows scammers to be more persuasive, increasing the likelihood of a successful scam.

Tactics Scammers UseOnce scammers have made contact, they use a variety of tactics to manipulate victims into compliance. These tactics include building trust, leveraging fear and offering financial incentives. Scammers posing as trusted figures, such as employers or debt collectors, are particularly effective, according to the report. For example, 86% of job listing scam victims reported that the scammer posed as a potential employer.

Additionally, 83% of debt collection scam victims encountered scammers pretending to be legitimate collectors.

In some cases, scammers rely on coercion, particularly in identity theft or government benefit scams. Victims are often manipulated through threats or promises of financial gain, making it harder for them to resist.

According to the report, younger consumers are more likely to report experiencing a wide range of manipulative tactics, suggesting scammers adapt their strategies based on the perceived vulnerability of the target.

The post 30% of US Consumers Fall Victim to Financial Scams appeared first on PYMNTS.com.